Stock Analysis

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, NVIDIA Corporation (NASDAQ:NVDA) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for NVIDIA

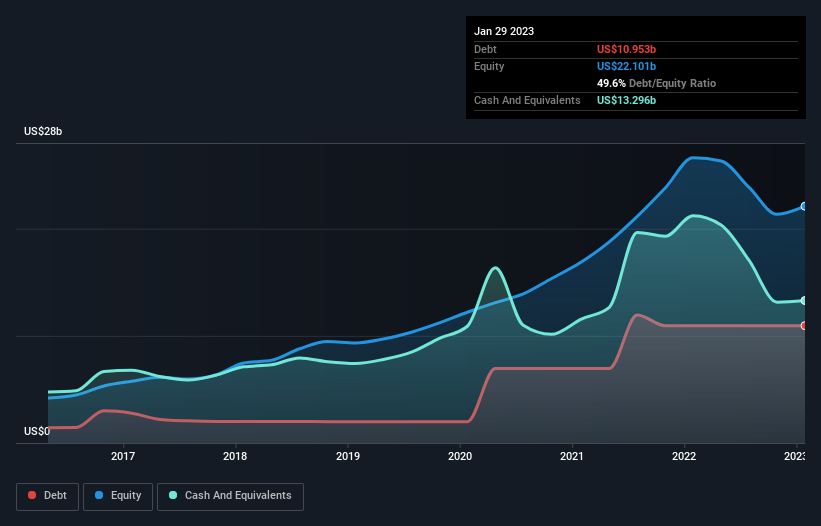

What Is NVIDIA's Debt?

The chart below, which you can click on for greater detail, shows that NVIDIA had US$11.0b in debt in January 2023; about the same as the year before. However, it does have US$13.3b in cash offsetting this, leading to net cash of US$2.34b.

How Strong Is NVIDIA's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that NVIDIA had liabilities of US$6.56b due within 12 months and liabilities of US$12.5b due beyond that. Offsetting these obligations, it had cash of US$13.3b as well as receivables valued at US$3.83b due within 12 months. So its liabilities total US$1.96b more than the combination of its cash and short-term receivables.

This state of affairs indicates that NVIDIA's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the US$666.9b company is short on cash, but still worth keeping an eye on the balance sheet. While it does have liabilities worth noting, NVIDIA also has more cash than debt, so we're pretty confident it can manage its debt safely.

In fact NVIDIA's saving grace is its low debt levels, because its EBIT has tanked 44% in the last twelve months. Falling earnings (if the trend continues) could eventually make even modest debt quite risky. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if NVIDIA can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While NVIDIA has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, NVIDIA generated free cash flow amounting to a very robust 82% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Summing Up

We could understand if investors are concerned about NVIDIA's liabilities, but we can be reassured by the fact it has has net cash of US$2.34b. And it impressed us with free cash flow of US$3.8b, being 82% of its EBIT. So we don't have any problem with NVIDIA's use of debt. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 3 warning signs for NVIDIA you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

What are the risks and opportunities for NVIDIA?

NVIDIA Corporation provides graphics, and compute and networking solutions in the United States, Taiwan, China, and internationally.

Rewards

Earnings are forecast to grow 30.99% per year

Earnings grew by 33.1% over the past year

Risks

Significant insider selling over the past 3 months

Further research on

NVIDIA

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:NVDA

NVIDIA

NVIDIA Corporation provides graphics, and compute and networking solutions in the United States, Taiwan, China, and internationally.

Exceptional growth potential with outstanding track record.