Stock Analysis

Key Insights:

-

Coca-Cola is one of the world's most recognizable brands as well as one of the oldest listed companies.

-

Its core business is very mature and operates in a market that's growing very slowly - however, the company has divested itself of low-margin bottling assets and is diversifying into new product segments which could help it keep EPS growing.

-

Weighing up these competing catalysts will help you build a narrative around the investment case for Coca-Cola.

Overview

Coca-Cola is the world’s largest non-alcoholic beverage company and operates in over 200 countries. The bulk of its revenue comes from Coca-Cola and other carbonated soft drinks, but Coke also owns 200 other brands in various product segments.

Coke’s core business model is to sell concentrated syrup to bottling companies that add water and carbonation, bottle, and distribute the finished product. There are approximately 225 of these bottling companies operating 900 plants around the world, and Coke owns a stake in many of them. As of 2021, the five largest bottling partners accounted for 41% of the total unit case volume.

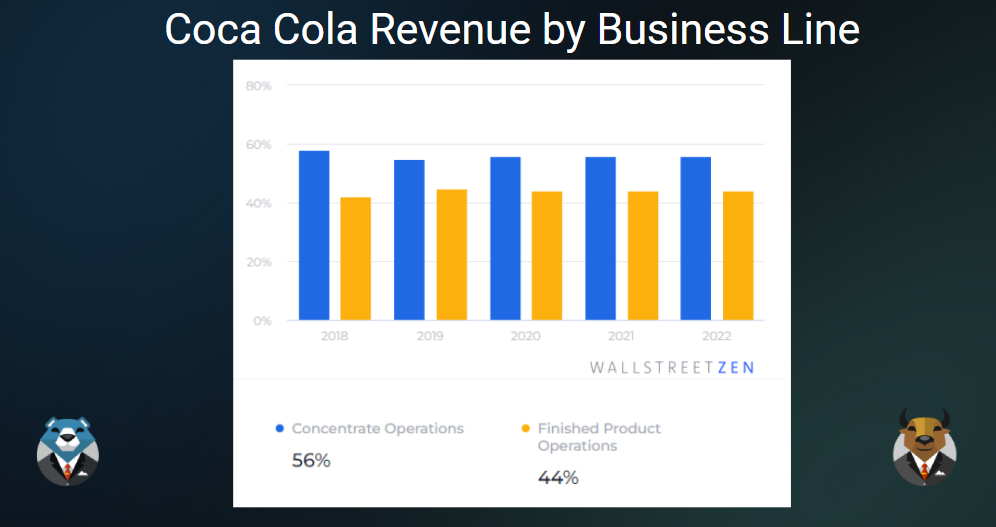

Concentrate sales account for approximately 55% of total revenue and 82% of case volumes. The remaining 45% of revenue and 18% of case volumes come from finished products which include other beverages.

The company is becoming increasingly diversified and is expanding its product lines to include health drinks, energy drinks, coffee, tea, and water.

Coke is well known for its dividend which has been raised annually for the last 61 consecutive years and currently yields 3%.

Recent History and Strategy

Coca-Cola’s financial performance over the last 15 years has not been impressive, with both revenue and net income just about flat. Over the last five years, performance has been considerably better. Some key developments between 2010 and 2020 give those trends context.

-

In 2010 Coca Cola acquired the North American bottling and distribution assets of Coca-Cola Enterprises, the main bottler in the US and Europe. This resulted in higher revenue, but lower margins for Coca-Cola (as bottling is a low-margin business.)

-

Then in 2014, the company began a major restructuring program which included selling those bottling assets and reducing headcount worldwide. This program initially resulted in higher costs, but ultimately led to improved margins.

-

In 2017, Coca-Cola paid an additional $3.6 billion in tax on repatriated offshore earnings due to changes to the US tax code. This combined with restructuring charges, falling revenue, and margins resulted in earnings falling 80% to a 17-year low.

-

The company has also localized its strategy for each region and market. Pricing in particular is market dependent. In developed markets prices have been raised substantially with little effect on revenue. However, in developing markets price increases have been minimized while Coke develops its distribution channel.

Strengths and opportunities

Brand, Scale, and Distribution Networks

The Coca-Cola Company’s historical success has come from a combination of its brand, scale, and distribution network.

As you are probably aware, Coca-Cola is one of the best-known brands in the world, and arguably the top beverage brand. For every Coke product, there are cheaper alternatives available almost everywhere, but Coke’s products are often viewed as the ‘real thing’ or a premium alternative. Coke’s massive scale allows it to spend billions on advertising to maintain that product positioning amongst consumers. This also allows Coke to charge a premium over competing brands.

Coke also has one of the biggest distribution networks in the world which has taken over a century to develop. This includes bottling plants, logistics, and relationships with wholesalers and retailers. Competitors can’t achieve Coke’s scale without replicating these distribution networks - and without that scale, they can’t hope to out-advertise Coke. Even Pepsi which has tried outspending Coke on marketing has had to accept second place in nearly every market in which the two compete.

Business Model and Restructuring

Coca-Cola’s business model and the restructuring over the last few years have resulted in improved revenue growth and margins.

By focusing on the high-value concentrate, or syrup, the company can maintain control of the product without investing in the entire supply chain. The recipe for Coca-Cola is a closely guarded secret, so the syrup is like intellectual property, and selling the syrup to bottling partners is like licensing that IP.

This business model is ‘capital light’ as the company doesn’t have to invest as much in bottling plants, warehouses, trucks, packaging materials, and inventory. It enabled Coke to maintain net income and free cash flow margins of over 20%, compared to 3.8% for the US consumer defensive sector. Because Coke’s cash flows are relatively stable, it can use debt effectively which has helped it achieve a return on equity of over 35% for the last 5 years. And the strong cash flows mean it can pay a 3% dividend.

In the last decade, the company has doubled down on the strategy by selling more of the wholly owned bottling companies. Coca-Cola has also localized its pricing strategies to increase revenue when possible or develop a market and distribution network where appropriate.

This has allowed the company to increase revenue in the North American market despite falling soda sales. Since 2017 total revenue increased by 19% while volumes grew just 12%.

New Product Opportunities

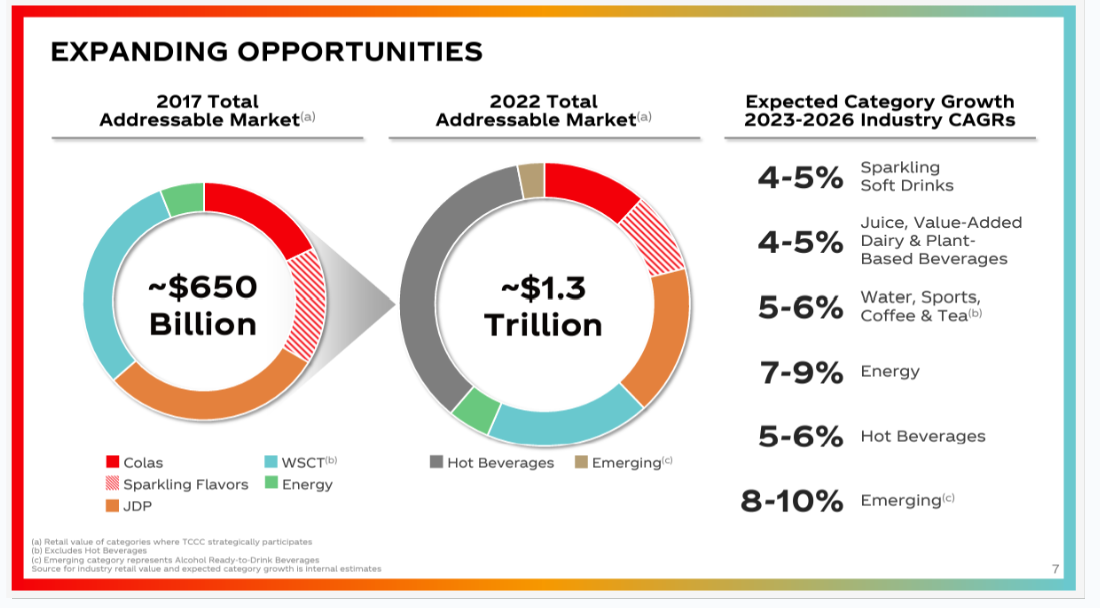

The first growth opportunity for Coca-Cola is its new product segments. By adding new product segments the company is growing its total addressable market and can reduce its reliance on carbonated soft drinks.

The new product categories include:

-

Hot beverages

-

Iced tea and coffee

-

Juice, dairy, and plant-based drinks

-

Bottled water

-

Energy drinks and sports drinks

-

Mixed alcoholic drinks

The product portfolio is being expanded via acquisitions and partnerships. In 2018 Coke acquired Costa Coffee, the UK’s leading chain of coffee shops. It also has a partnership with Monster Beverage Corp to distribute energy drinks globally.

Developing Market Opportunities

Coca-Cola’s recent revenue growth has mostly come from its North American market where it has raised prices. Elsewhere the company has focussed on developing the market. These other markets and particularly emerging markets will be a key area for growth in the future.

Weaknesses, risks, and threats

Coca-Cola is a Very Mature Company with a Shrinking Market

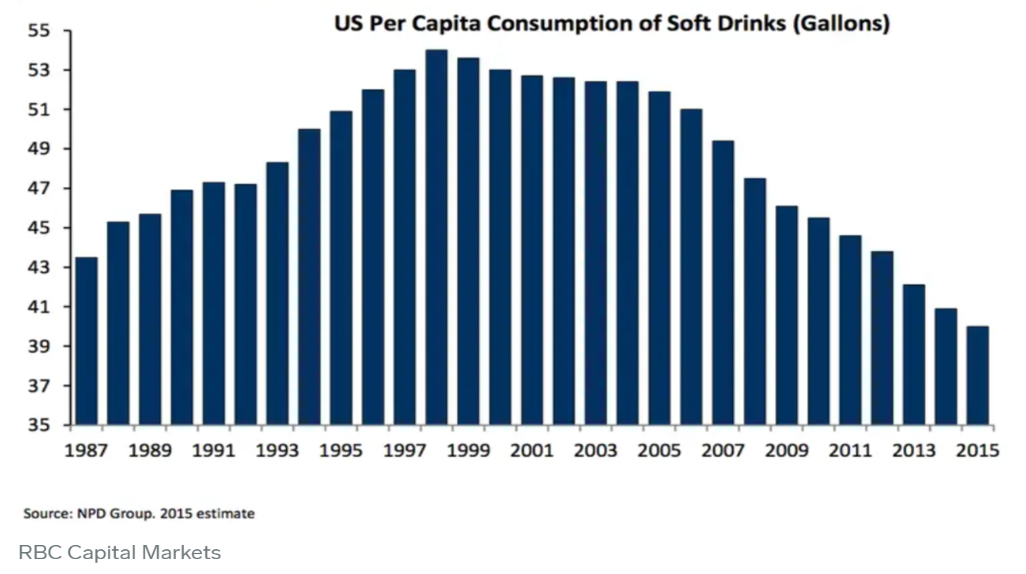

The first weakness we will look at is the fact that Coca-Cola is now a very large and mature company, and potentially ‘ex-growth’. At the same time, the company is fighting a trend toward healthier eating and away from products that contain sugar.

There’s a strong correlation between the consumption of sugar-sweetened drinks and obesity. This isn’t entirely due to soft drinks as the correlation also holds for increases in GDP and other factors - but sugar consumption is viewed as something that can be addressed. Over 50 countries have already introduced new taxes on sugar-sweetened drinks.

The diet versions of Coca-Cola’s products have been relatively successful. But consumers aiming for a healthier diet may try to avoid soft drinks altogether. This is why the company is adding different market segments to its portfolio.

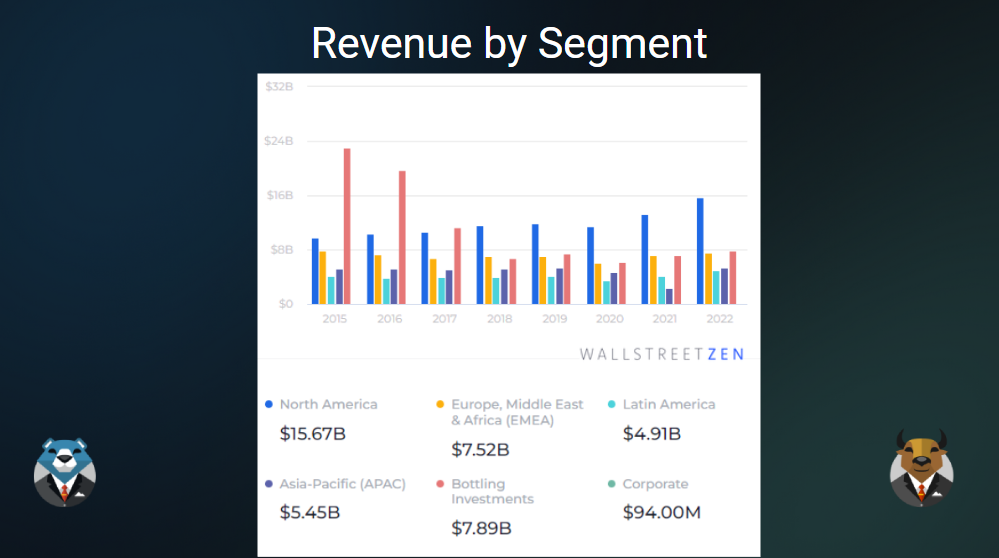

Beyond the reliance on carbonated beverages, North America, which is a very mature market, is still the largest revenue contributor and has been responsible for most of Coke’s revenue growth in recent years. It’s likely that future growth will depend on Coke’s ability to grow revenue in other markets and product segments.

The gross margin has fallen over the last 14 years, while the bottom line margins have remained flat. This may reflect the fact that Coca-Cola has reached ‘peak efficiency’ and is no longer benefiting from its scale.

Limited Advantage in Some New Markets

To overcome the challenges outlined above, Coca-Cola is diversifying its product portfolio. The financial results are somewhat opaque when it comes to the share of the revenue from various product lines - but the core carbonated beverage brands appear to still account for around 70% of revenue.

One of the reasons for the slow growth from other segments is that the company doesn’t necessarily have a competitive advantage in other segments. It can probably leverage its distribution networks for sports and energy drinks and bottled water - but it doesn’t have the brand advantage of Coca-Cola, Fanta, and Sprite. This is likely the reason it has partnered with Monster Beverage, a leading energy drink brand.

When it comes to hot coffee, tea, and health products, the company has even less of an advantage. To see success in these segments Coke may need to form new partnerships or make acquisitions - although regulators may block acquisitions.

Several Significant Risks

There are a few significant risks that Coca-Cola’s shareholders should be aware of:

Tax

Coca-Cola has an ongoing tax dispute with the US IRS. The dispute involves taxes due on foreign income dating back as far as 2007. In 2020 a court ruled that the company owed an additional $3.3 billion but the decision was appealed, and the case was put on hold pending the decision from another similar case. Theoretically, the amount owed could be as high as $14 billion if the ruling is applied to the years from 2010 to 2022 , however, this could again be appealed and drag on for longer. To give this amount some context, it equates to around 4% of the market capitalization and 130% of net income. The company currently has just $400 million set aside to settle this liability.

Dividend

Coke is well known for its dividend, which has been increasing annually for 61 years. However, there is a risk that the payout ratio is becoming unsustainable while there is probably a lot of pressure to keep raising it - what message would it send to investors if the dividend wasn’t raised?

Currency effects

More than 50% of Coca-Cola’s revenue and operating income comes from outside of the US. So, when the USD strengthens against other currencies, this results in lower earnings. This can of course go the other way - but leads to earning volatility nonetheless.

Interest rates

Coca-Cola has significant debt, with a debt-to-equity ratio of 160%. This isn’t necessarily a problem as cash flows are quite reliable. However, it does mean changes in interest rates can have a large impact on net income. Fortunately, most of the company’s debt matures after 2027 so the risk is low in the near term.

Current valuation and context

We’ll start by looking at the current share price and what it reflects about the market’s expectations for the company. The current share price of $60 implies an EPS growth rate of around 12.8%.

To give that growth rate some context, let’s look at recent growth trends. Over the last five years, earnings have increased by 21% - however, that’s somewhat misleading as the company paid a large, one-off tax on foreign earnings in 2017. Over four and six years, annual earnings growth has been in the 6 to 10% range. So 12.8% is slightly higher than historical growth rates.

The Bull Case

Okay, now let’s look at the more bullish forecasts and the narratives that might support them. At the top of the range, analysts are expecting EPS growth as high as 18.9% for 2023, followed by growth in the low teens.

We can summarize the three most bullish narratives as follows:

The business strategy and restructuring will continue to pay off:

-

Coca-Cola has divested itself of many of its low-margin bottling plants.

-

Margins should therefore stay at the upper end of the recent range.

-

The company is also increasing prices where it can.

-

This means revenue can increase even if volumes remain flat.

Growth from the new product segments will accelerate:

-

Coca-Cola has entered several new product segments

-

Contribution from these segments is relatively small - but represents a large opportunity

-

Growth from these segments will offset falling CSD (carbonated soft drink) sales.

Growth in emerging markets will accelerate:

-

Recent revenue growth has mostly come from North America, with all the other markets lagging.

-

One of the reasons is that Coca-Cola has raised prices in North America, but concentrated on growing its brand and distribution in other markets

-

As this strategy begins to pay off, growth from outside of North America (representing 55% of sales) will accelerate

The Bear Case

Looking at the more bearish forecasts, some analysts expect EPS growth to be as low as 8% - which would imply a fair price would be about $49 and 25% below the current price.

Some of the narratives that would support a bearish outlook include:

Most of Coke’s business is exposed to a very mature market:

-

Approximately 70% of revenue comes from carbonated soft drinks.

-

CSD sales are declining as the world moves away from sugar and toward healthier drinks.

-

Coke’s market share is already high, leaving little space to grow by winning market share.

-

Long-term revenue growth is likely to be very low.

Limited advantage in new product categories:

-

While the company is actively diversifying into new product categories, penetration in these new segments has been low.

-

Coke doesn’t have the same advantages it has with its classic brands in these new segments.

-

Its ability to make acquisitions in these new segments will be blocked by regulators.

-

Opportunities for new sources of revenue are limited and can’t offset the loss of growth in the CSD market.

There are a number of significant risks:

-

The ongoing dispute with the IRS could result in a $14 billion tax bill

-

Coca-Cola is exposed to currency and interest rate risk

-

The dividend may be unsustainable

-

The valuation needs to take these risks into account.

Key Questions

To help you build a narrative of your own, you can ask yourself the following questions:

- Do I think the localized pricing strategy will allow them to continue increasing prices steadily in mature markets, and growing emerging markets?

- If so, how will this impact revenue growth?

- If so, how will this impact revenue growth?

- Do I think the company will be able to generate revenue growth in its new segments to make up for the decline in CSD consumption?

- If so, how will they contribute to future revenue?

- Do I think emerging markets will provide revenue growth that maturing markets can’t?

- If so, how much will they contribute?

- If so, how much will they contribute?

- Do I believe the dispute with the IRS will result in a huge tax bill?

- If so, how much could it be (between $400m and $14bn?)

- If so, how much could it be (between $400m and $14bn?)

- Do I believe the company's current debt load is manageable?

- If so, will its profit margins be impacted severely by higher interest rates if it refinances existing loans?

You can use your answers to these questions, as well as further research, to start building your own narrative and valuation for Coca-Cola. For key financial data, have a look at the Simply Wall Street report for Coca-Cola . This report now includes a Notes feature to help you record and track your narrative for the company.

You can also use the Simply Wall St stock valuator (currently in beta) to estimate a fair value for Coca-Cola based on your own assumptions for earnings growth and an appropriate discount rate.

References:

- Coca-Cola Investor Relations

- Market US Coke Facts

- Investors Chronicle

- Wallstreetzen

- Verified Market Research

- Grand View Research

- WHO

- Obesity evidence hub

- WSJ on the 2014 restructuring plan

- Business Insider on declining soda sales

What are the risks and opportunities for Coca-Cola?

The Coca-Cola Company, a beverage company, manufactures, markets, and sells various nonalcoholic beverages worldwide.

Rewards

Trading at 24.6% below our estimate of its fair value

Earnings are forecast to grow 6.88% per year

Earnings have grown 11% per year over the past 5 years

Risks

Has a high level of debt

Further research on

Coca-Cola

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.

About NYSE:KO

Coca-Cola

The Coca-Cola Company, a beverage company, manufactures, markets, and sells various nonalcoholic beverages worldwide.

Established dividend payer and good value.